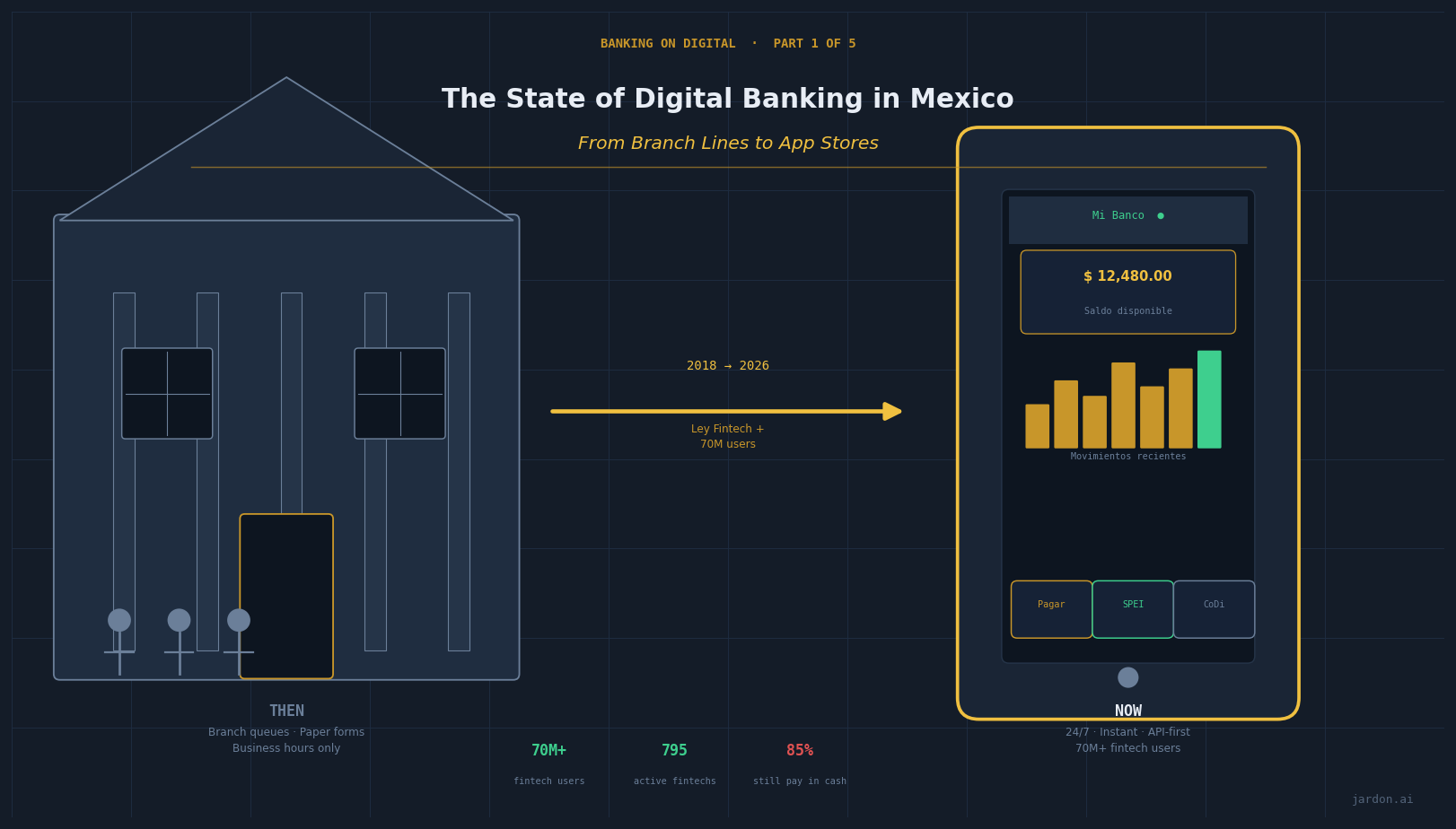

Digital banking in Mexico, from branch lines to app stores

Mexico has 70+ million fintech users, a landmark Fintech Law, and a national digital finance strategy through 2030. So why does 85% of the population still pay for their morning tacos in cash? Welcome to the most fascinating contradiction in Latin American finance

Part 1 of 5

"The future is already here, it's just not evenly distributed". William Gibson.

Mexico is, by almost every metric, a fintech juggernaut in the making. It is the second-largest economy in Latin America, home to +130 million people, with a smartphone penetration that would make some European markets blush. Yet walk into any corner tianguis or little town on any given Sunday morning and you'll find something remarkably consistent: cash. Lots of it.

This is not a story of failure. It is a story of transformation in progress: messy, fast, uneven, and genuinely exciting for anyone who understands what is actually happening beneath the surface.

Banking on Digital is a five-part series that unpacks Mexico's digital banking revolution from both a technical and business perspective.

Where do we stand today?

The Fintech Surge

Mexico's fintech ecosystem has experienced an explosive growth over the past decade. As of end of last year,795 active fintechs operate in the country, a figure that has more than doubled since 2019 when 394 companies were registered. More than half of these focus on digital payments and credit, which tracks perfectly with where the demand is.

The user numbers are equally striking. Over 70 million Mexicans now use fintech services, and projections point to 86 million users by 2027. To put that in perspective: that's roughly the entire population of Germany adopting fintech in a single country, in under a decade.

It seems great right? Mmm, let's look at the other face of the coin.

Fewer than 70% of Mexican adults have a formal bank account. More than 50% of Mexican companies have never applied for a formal loan. And 85.2% of adults still use cash as their primary payment method for everyday purchases under 500 pesos (about 25 dollars).

That is not a rounding error. That is a structural reality that defines both the challenge and the opportunity facing every player in this market.

How do you reconcile 70 million fintech users with 85% cash dependency? The answer is nuanced, and it gets to the heart of what makes Mexico such a fascinating laboratory for financial innovation.

How Mexico Compares Internationally

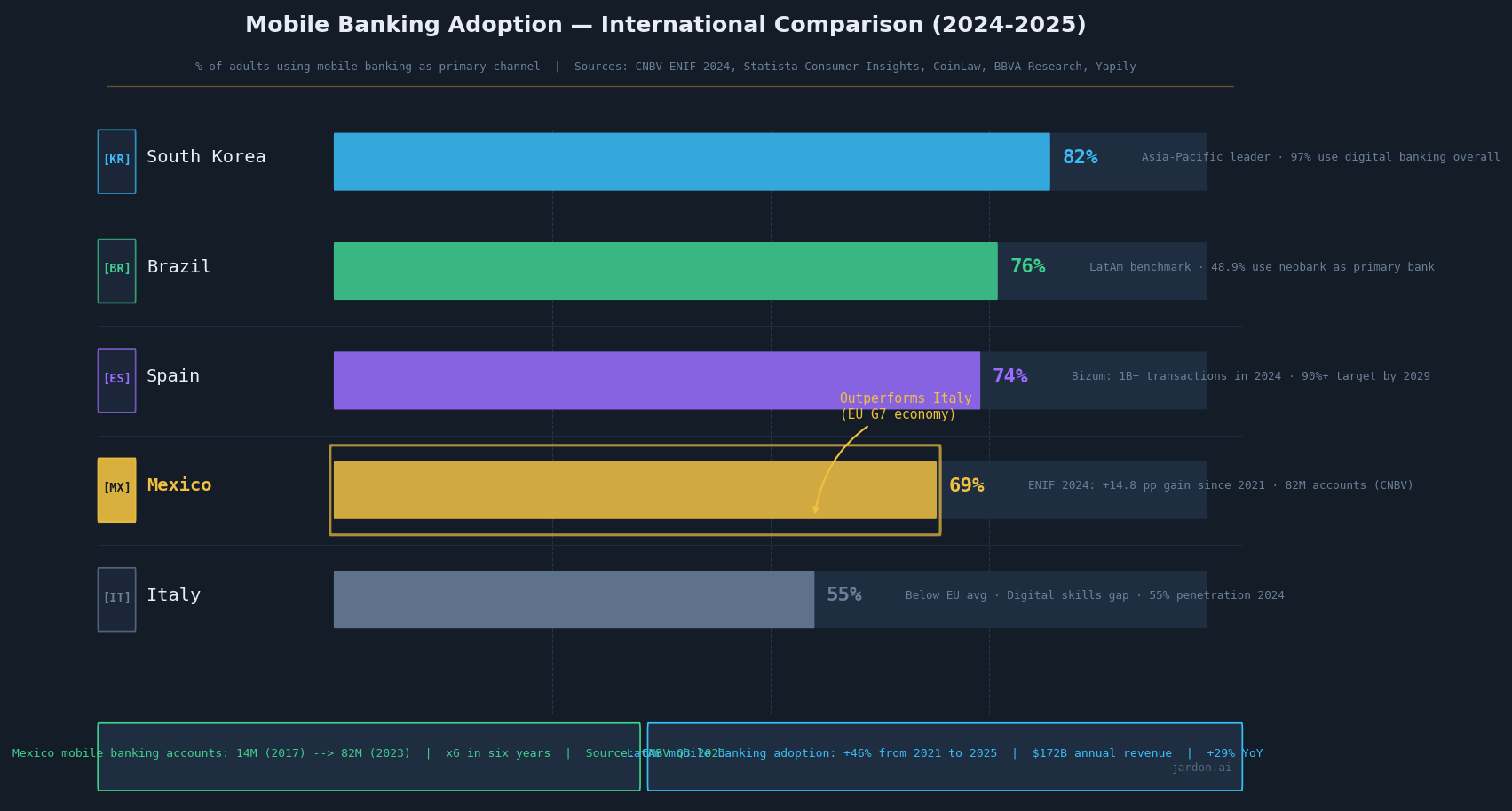

Mexico's 69.1% mobile banking adoption rate, measured by the ENIF 2024, places it in genuinely competitive territory globally. South Korea leads at 82%, Brazil, Mexico's most direct regional peer, sits at 76%, and Spain, one of Europe's more digitally advanced economies, registers around 74%. But the number that should stop you mid-scroll: Mexico at 69% outperforms Italy at 55% , a G7 economy, a founding EU member, with GDP per capita nearly three times higher.

This is not an accident. It reflects the leapfrog dynamic that defines Mexico's digital trajectory. When traditional banking infrastructure is underdeveloped, consumers skip the intermediate steps and go straight to mobile. Italy built a dense branch and ATM network for decades; Mexican consumers, with fewer alternatives, embraced the smartphone as their primary financial device out of necessity, and that necessity is becoming an advantage.

The growth trajectory reinforces the point. According to CNBV data, Mexico had 14 million mobile banking accounts in Q3 2017. By Q3 2023 that figure had reached 82 million, a six times increase in six years. Latin America as a region recorded 46% mobile banking adoption growth between 2021 and 2025, generating $172 billion in annual revenue with 29% year-over-year expansion. Mexico, alongside Brazil and Colombia, is driving that regional number.

The gap with Brazil (76% vs 69%) is real and worth understanding. Brazil benefits from a more mature neobank ecosystem, Nubank alone serves over 100 million customers across Latin America, and from Pix, its instant payment system that achieved adoption speed that made Mexico's CoDi look like it was moving through regulatory quicksand. Brazil's Pix processed over 42 billion transactions in 2023. CoDi, after six years, had processed 11.9 million cumulative transactions. The lesson for Mexico is not that the technology failed, it is that adoption requires ecosystem alignment, not just infrastructure deployment.

The Digital Infrastructure Gap

Part of the answer lies in connectivity. 83.1% of individuals aged 6 and above use the internet, but break it down geographically and the fault line becomes visible: 86.9% penetration in urban areas versus 68.5% in rural zones , an 18.4 percentage point gap that maps almost perfectly onto financial exclusion patterns.

The implication is clear: digital banking in Mexico is not primarily a product problem or a technology problem. It is an infrastructure and trust problem, and solving it requires a fundamentally different approach than what worked in London, Singapore, or São Paulo.

How We Got Here: A Brief History of Mexican Banking Digitization

Understanding the present requires at least a glance in the rearview mirror. Mexican banking digitization did not happen overnight, and the path was anything but linear.

Phase 1: The Pre-Digital Era (Pre-2010)

For most of the 20th century, Mexican banking was a highly concentrated, oligopolistic industry. A handful of large institutions, many with foreign parent companies after the 1994 crisis and subsequent privatizations, controlled the vast majority of assets. Branch networks were dense in major cities, and with almost no presence everywhere else. If you were not in the formal economy, you were effectively outside the financial system. Plus, a natural lack of confidence on the banking system due to the cyclical financial crisis on the country, derived on low penetration on the general population on using any banking product. There is tradition in Mexico of our grandfathers of keeping the money under the mattress.

The result was predictable: low inclusion rates, high fees, and a population that had rational, experience-based reasons to distrust formal financial institutions.

Phase 2: The Mobile Inflection Point (2010–2017)

The proliferation of smartphones changed the tendency. By 2017, Mexico had reached sufficient smartphone penetration to make mobile-first financial products economically viable at scale. Early digital banking products from traditional institutions , began to appear.

This period also saw the emergence of the first wave of Mexican fintechs: scrappy, undercapitalized, regulatory gray-area companies trying to serve the underserved. They were operating in a legal vacuum, which created both opportunity and risk.

Phase 3: The Regulatory Leap (2018–2022)

In March 2018, Mexico made a move that positioned it as a pioneer in global financial regulation: the publication of the Ley para Regular las Instituciones de Tecnología Financiera, known universally as the Ley Fintech. Drafted by SHCP, supervised by CNBV and BANXICO, the law established the legal framework for fintech institutions, electronic payment funds, and the foundational architecture for what would eventually become Open Banking in Mexico.

This was not perfect legislation, no landmark regulation ever is on day one. But it sent an unambiguous signal: Mexico was not going to regulate fintech into irrelevance. The sandbox was open.

The law's impact was immediate and compound. Fintechs that had been operating in regulatory ambiguity could now formalize. New entrants, including significant international players, had a legal framework to work within. CNBV began issuing formal fintech licenses, and the quality of the ecosystem began to improve.

Phase 4: Acceleration and Market Maturation (2022–Present)

This is the phase we are living through today, and it is moving fast.

Use of banking apps to manage accounts jumped from 54.3% in 2021 to 69.1% in 2024, a 15-point gain in three years that reflects genuine behavioral change, not just technology adoption. The unbanked population is contracting, though slowly. The share of adults with no savings at all fell from 39.8% in 2021 to 33.6% in 2024, still high in absolute terms, but tendency is clear.

Meanwhile, the regulatory environment has continued to evolve. In July 2024, the CNBV introduced new regulations specifically targeting fraud prevention within banking institutions, requiring comprehensive internal controls, real-time monitoring frameworks, and enhanced standards. This reflects the growing complexity and attack surface of a rapidly digitalizing financial system.

The Infrastructure Layer: SPEI, CoDi, and DiMo

No discussion of Mexican digital banking is complete without acknowledging the base of the pyramid: the payment infrastructure that underpins the entire ecosystem.

SPEI: The Workhorse

SPEI (Sistema de Pagos Electrónicos Interbancarios) is Banxico's real-time gross settlement system and, quietly, one of the most important pieces of financial infrastructure in Latin America. Operating 24/7/365, SPEI processes interbank transfers in seconds and forms the backbone of virtually every digital payment in Mexico, including those executed by fintechs, neobanks, and traditional institutions alike.

If Mexico's fintech ecosystem is a city, SPEI is the electrical grid. You may not see it, but nothing works without it. And let's give a praise to it, in conversations with Canadians and US citizens, they recognize that is marvelous to be able to receive money on the same day that is transfered.

CoDi: The Lesson in Adoption Friction

CoDi (Cobro Digital) was launched in 2019 as Mexico's QR-code-based instant payment system, built on top of SPEI. The ambition was bold: 18 million registered users within the first year. Yeah I have being on projects that overestimate the impact.

The reality was more instructive than impressive. By September 2025, six years after launch, CoDi had accumulated 21.8 million validated accounts and just 17.8 million cumulative transactions. Total volume over six years reached 16.72 billion pesos, averaging roughly 875 pesos per transaction.

Why did CoDi underperform? A perfect storm of adoption friction: merchants and users preferred existing SPEI rails, and banks had no commercial incentive to promote CoDi because it generates zero commissions. It's always business right? What about clients?

This is a case study in why technically superior products do not automatically win markets. Incentive alignment matters as much as engineering quality. Every fintech product manager in Mexico should have this burned into their memory.

DiMo: The Second Attempt

DiMo (Dinero Móvil) represents Banxico's evolved approach: phone-number-based transfers over SPEI rails, eliminating the need to remember 18-digit CLABE numbers. Early adoption signals are more encouraging than CoDi, partly because the user experience addresses actual friction points, and partly because lessons were learned. This model is more similar to Chinese to Indian model where electronic transactions penetration is highly tied to the mobile usage.

The Players: A Market in Full Transformation

The competitive landscape of Mexican digital banking today is genuinely complex , and that complexity is a feature, not a bug.

Traditional banks are no longer sleeping. Several have made genuine, meaningful investments in digital transformation, not just putting a mobile app on top of a 30-year-old core, but rethinking customer journeys, APIs, and data architectures from the ground up. The ones doing it right deserve acknowledgment: building modern digital capabilities inside a regulated, legacy-burdened institution is significantly harder than it looks from the outside.

Neobanks and challengers have demonstrated that it is possible to onboard millions of users at low cost, process credit decisions in minutes rather than weeks, and build products that people actually want to use. The numbers speak for themselves: one major neobank operating in Mexico granted its ten millionth loan in January 2025. Another, operating through a retail distribution network, had 12 million clients onboarded by September 2024. These are not pilot programs. These are at-scale operations.

SME-focused lenders are tackling one of the most persistent gaps in Mexican finance: credit access for small businesses. Digital lending platforms disbursed over 17 billion pesos to approximately 80,000 SMEs in 2024–2025, using algorithmic credit assessment to reduce approval times from weeks to minutes.

Open Banking infrastructure players are building the connective grid: APIs, data aggregation layers, and identity verification tools. Mexico's open banking model now involves over 80 financial institutions, governed by the Fintech Law framework.

The Regulatory Horizon: 2025–2030

Perhaps the most significant recent development is not a product launch or a funding round. It is a strategic signal from the Mexican government itself.

A National Digital Finance Strategy (2025–2030) has been launched by Mexico's financial authorities, establishing a roadmap explicitly designed to position Mexico as the digital financial hub of Latin America by 2030.

The strategy encompasses regulatory modernization, open banking expansion, digital identity infrastructure, and inclusion-focused initiatives. Importantly, it acknowledges that seven years after the Fintech Law, a regulatory reform is expected to create a more flexible and collaborative framework, recognizing that the original 2018 regulation, while groundbreaking, needs to evolve alongside the market it governs.

From a technology perspective, this roadmap has direct implications for anyone building or running digital financial platforms in Mexico: the regulatory environment is going to keep moving, and adaptability is not optional.

Next on these series: Open Banking & APIs.

Sources & References

Facephi Observatory — Financial Inclusion in Mexico 2026: Fintech, Digital Payments, and Neobanks (March 2026). https://facephi.com/observatory/en/financial-inclusion-mexico-fintech-digital-payments/

Chambers and Partners — Fintech 2025: Mexico (March 2025). https://practiceguides.chambers.com/practice-guides/fintech-2025/mexico

CoinLaw — Open Banking Adoption Statistics 2025 (March 2026). https://coinlaw.io/open-banking-adoption-statistics/

CoinLaw — Fintech Adoption Statistics 2026 (March 2026). https://coinlaw.io/fintech-adoption-statistics/

Open Banking Excellence — Mexico in Focus: Open Banking and Financial Inclusion (January 2025). https://www.openbankingexcellence.org/blog/mexico-in-focus-open-banking-and-financial-inclusion

Infomineo — How Fintech Is Transforming Financial Inclusion in Mexico (June 2025). https://infomineo.com/financial-services/how-fintech-is-transforming-financial-inclusion-in-mexico/

The Business Year — The Truth About Mexico's Financial Exclusion — And How Fintech Is Fixing It (March 2025). https://thebusinessyear.com/article/the-truth-about-mexicos-financial-exclusion-and-how-fintech-is-fixing-it/

Statista — Digital Banks: Mexico Market Forecast. https://www.statista.com/outlook/fmo/banking/digital-banks/mexico

Banxico — Ley para Regular las Instituciones de Tecnología Financiera (Official text). https://www.banxico.org.mx

BBVA Research — Mexico: Mobile Banking, the Future or the Present? (January 2024). https://www.bbvaresearch.com/en/publicaciones/mexico-mobile-banking-the-future-or-the-present/

BBVA Research — Mexico: Digital Financial Inclusion Shows Progress in 2024 (June 2025). https://www.bbvaresearch.com/en/publicaciones/mexico-digital-financial-inclusion-shows-progress-in-2024

CoinLaw — Mobile Banking Statistics 2025 (January 2026). https://coinlaw.io/mobile-banking-statistics/

Statista Consumer Insights — Mobile and Online Banking Penetration by Country 2025. https://www.statista.com/statistics/1440760/mobile-and-online-banking-penetration-worldwide-by-country/

Yapily — Open Banking in Europe: A 2025 Market Overview. https://www.yapily.com/blog/open-banking-in-europe

Market.biz — Mobile Banking Statistics 2026 (March 2026). https://market.biz/mobile-banking-statistics/

El CEO — Revolut, Nu, Klar, Oxxo Bank: la batalla por ser el neobanco fuerte de México (December 2025). https://elceo.com/negocios/revolut-nu-klar-oxxo-bank-mercado-pago-la-batalla-por-ser-el-neobanco-fuerte-de-mexico/

Legal Paradox — Mexican Neobanks Market Analysis 2026. https://www.legalparadox.com/insights/mexican-neobanks-market-share-2026

Nu Holdings — Form 6-K FY2025 Results (SEC Filing, February 2026). https://www.sec.gov/Archives/edgar/data/0001691493/000129281426000501/nu20260225_6k.htm

Expansión — Más digital, menos tradicional; así se reconfigura la banca en México (November 2025). https://expansion.mx/economia/2025/11/21/mas-digital-menos-tradicional-reconfigura-la-banca-en-mexico

IT Masters Mag — Fintech: El rival inesperado de los bancos tradicionales (January 2025). https://www.itmastersmag.com/transformacion-digital/todo-sobre-las-fintech-el-rival-que-los-bancos-no-querian/